The California to Colorado Home Equity Transfer: A Step-by-Step Guide

Last Updated: March 2026 | By Nick Ahrens, North Denver Report

The average California homeowner is sitting on $603,000 in equity, more than double the national average. If you're one of them and you're thinking about moving to Colorado, that equity isn't just a number on a statement. It's a tool that can completely change what your next chapter looks like financially. Here's exactly how to use it.

Why California Equity Goes So Far in Colorado

The math here is striking. The median home in San Francisco sold for $1.5 million in February 2026 (Source: Redfin). The median home in Broomfield, a master-planned suburb 20 miles north of Denver with mountain views and top-rated schools, was approximately $647,000 in early 2026 (Source: Zillow). In Anthem, Broomfield's most established luxury community, the median sits around $1,027,238. In Anthem Highlands, it's approximately $615,000. In Baseline, Broomfield's newest development, homes start in the mid-$500s.

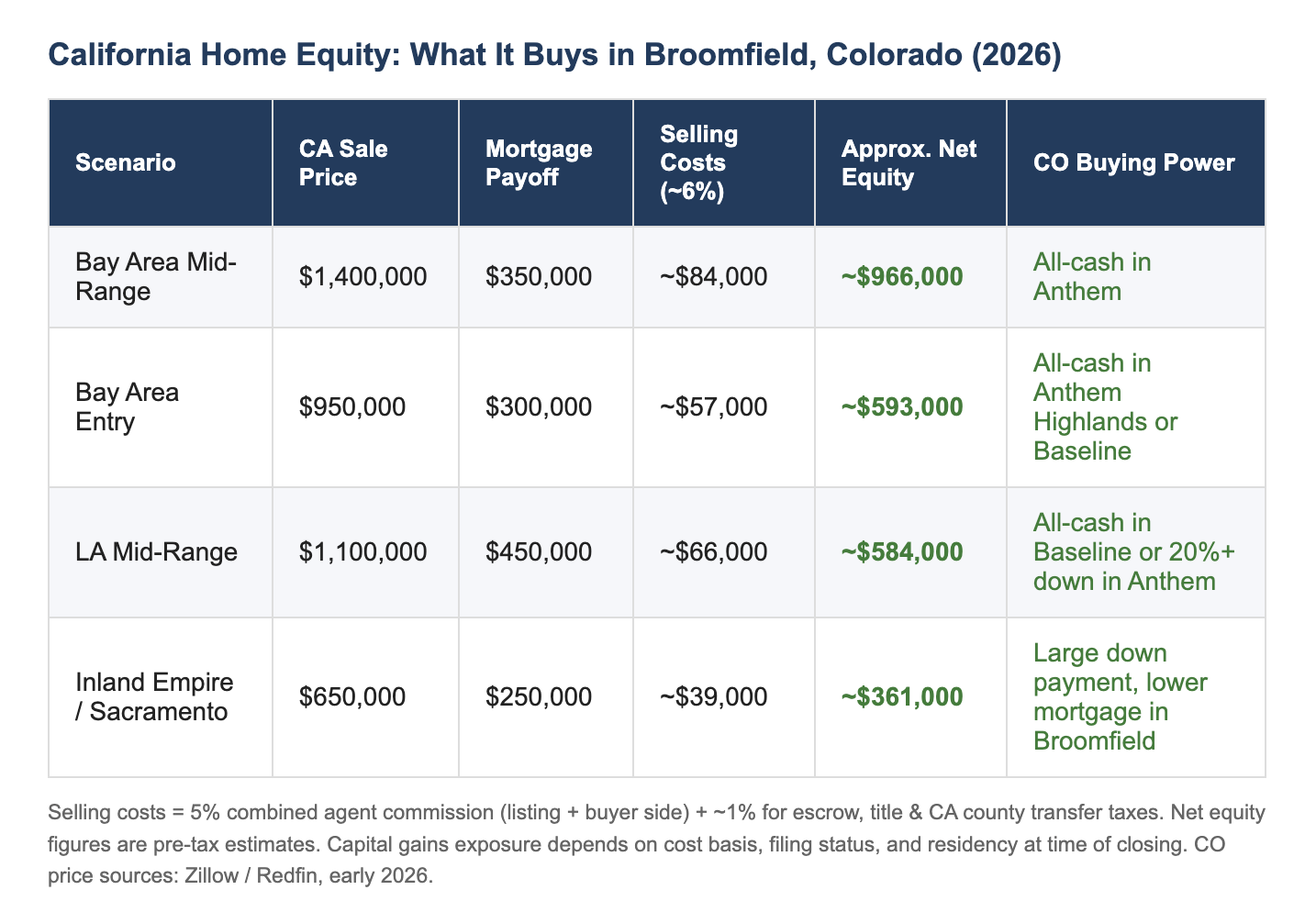

A Bay Area homeowner selling a $1.4M house with a $400,000 mortgage walks away with roughly $1 million in gross equity (before closing costs). In California, total selling costs typically run about 6% of the sale price, that's a 5% combined agent commission (listing side plus buyer side) plus roughly $14,000 in escrow fees, title insurance, and county transfer taxes. On a $1.4M sale, that's approximately $84,000 out the door, leaving a net equity of around $916,000. Many clients in that position can purchase a home in Broomfield outright: no mortgage. Zero monthly payment. For a remote tech worker earning a Silicon Valley salary in a Colorado tax environment, this is a fundamentally different financial life.

Step 1: Know Your Equity Position Before You Plan Anything

Before you call a Colorado real estate agent, call your California lender or run a quick estimate. Your equity is your home's current market value minus your outstanding mortgage balance. If your home is worth $1.4M and your remaining mortgage is $350,000, your equity is $1.05M gross.

But gross equity isn't what you net. California sellers typically pay around 6% in total transaction costs, a 5% combined agent commission plus another ~1% for escrow, title, and transfer taxes. On a $1.4M sale, that's roughly $84,000 in selling expenses before your mortgage payoff. Run the actual numbers early. That net equity figure is the starting point for everything else in your Colorado plan.

California homeowners hold an average of $603,000 in equity as of Q3 2025, more than double the national average of $299,000 (Source: Cotality, Q3 2025 Homeowner Equity Report). Even after a slight equity dip in 2025 (California homeowners lost an average of $33,000 year-over-year), the position is extraordinary compared to what that money can buy in Colorado.

Step 2: Understand the Tax Implications Before You Sell

This is where people get tripped up, and it's where a CPA with interstate relocation experience is non-negotiable.

Federal capital gains exclusion. If you've lived in your California home for at least 2 of the last 5 years, you can exclude up to $250,000 in gain from federal capital gains tax ($500,000 if married filing jointly). If your gain exceeds those thresholds, the excess is taxed at long-term capital gains rates, currently 0%, 15%, or 20% depending on your income.

California state income tax on the gain. California taxes capital gains as ordinary income, up to 13.3%. If you're still a California resident when you close the sale, California will tax your gain above the federal exclusion. For a tech worker with a $600,000 gain and a $500,000 married exclusion, that remaining $100,000 could face a state tax bill of $13,000 or more, just to California.

Timing your residency change. Here's where the strategy gets interesting. If you establish Colorado residency before your California sale closes, your California tax obligation on the capital gain may be significantly reduced or eliminated. Colorado's income tax is a flat 4.4% versus up to 13.3% in California. The difference on a $200,000 taxable gain is roughly $17,800 in tax savings. The mechanics of when you legally establish a new state domicile matter enormously. Talk to a CPA who has done this before, not a general practitioner.

Step 3: Decide on Your Sequencing Strategy

This is the most practical question: do you sell first, or buy first?

Sell California first, then buy Colorado. This is the lowest-risk approach. You know exactly what you're working with, you're not carrying two properties, and you can make a strong cash or large-down-payment offer in Colorado. The downside: you may need temporary housing in Colorado while you close, or you may feel pressure to accept whatever is available in the moment.

Buy Colorado first with a bridge loan. A bridge loan lets you borrow against your California equity to fund your Colorado purchase before your California home sells. This means you can make a non-contingent offer in Colorado, a significant advantage, without waiting. Bridge loans typically run 6–12 months and carry rates roughly 1–2% above a standard mortgage. They're short-term by design. Once your California home closes, you pay off the bridge loan and potentially refinance the Colorado home, or pay it down to your target amount.

Make a contingent offer. Least preferred in a competitive market, but still an option. You make an offer on a Colorado home contingent on the sale of your California home. Sellers in Colorado are generally less receptive to contingent offers, especially on desirable properties. In a softer market, this becomes more viable.

Most of my California clients opt for one of the first two paths. Which one makes sense depends on your timeline, your risk tolerance, and how quickly your California home is likely to sell.

Step 4: Run Your Colorado Buying Power Numbers

Here's a simplified version of the calculation I walk clients through:

Selling costs calculated at ~6% of sale price: 5% combined agent commission (listing + buyer side) plus ~1% for escrow, title insurance, and California county transfer taxes. Net equity figures are pre-tax estimates, your capital gains exposure depends on your cost basis, filing status, and residency at time of closing. Source for CO prices: Zillow/Redfin, early 2026.

Step 5: Understand What You're Buying in Colorado

If you're landing in Broomfield, you have three master-planned communities to consider, each with a distinct price point and vibe. For a deep dive, read The Definitive Comparison: Anthem vs. Anthem Highlands vs. Baseline.

Anthem is Broomfield's most established luxury community. Homes run from the high $600s to well over $2M. The community park is 22 acres, the pool complex is resort-level, and the mountain views are constant. This is where most of my Silicon Valley clients end up. Median price: ~$1,027,238 (late 2025).

Anthem Highlands sits just above Anthem, literally, it's at higher elevation with arguably better views. The price points are more accessible, typically $500K–$850K, with similar amenities. Average price: ~$615,000.

Baseline is Broomfield's newest development, still being built out. It has a more urban-adjacent feel with a planned town center, strong walkability for the area, and the lowest entry points of the three. Median: ~$566,000.

All three are within 25 minutes of Boulder, 30 minutes of downtown Denver, and 45 minutes of world-class skiing. For remote workers, this is the whole point.

Step 6: The IRS Migration Data Confirms This Is a Real Trend

This isn't just anecdote. IRS migration data shows that 144 tax returns per year flow from California into Broomfield County, with an average adjusted gross income of $125,764. From Santa Clara County specifically, Silicon Valley, the average AGI is $214,893, the highest of any incoming group (Source: IRS Migration Data, 2021–2022). These are households with real equity, real income, and real buying power.

They're not moving because they have to. They're moving because they ran the numbers and the numbers are undeniable.

The Bottom Line on California-to-Colorado Equity

If you own a home in California and you're thinking about Colorado, your equity is the most powerful financial tool in this move. The strategy is:

Know your net equity position (home value minus mortgage minus selling costs)

Talk to a CPA about your capital gains exposure and residency timing before you list

Decide on your sequencing (sell first vs. bridge loan)

Get pre-approved or pre-qualified in Colorado so you know exactly what you're working with

Connect with a local Broomfield agent who has done this move before, someone who knows the communities, the metro district nuances, and the typical California buyer's questions

That last part is where I come in.

Ready to run the numbers on your specific move?

The equity transfer is the part most California buyers get wrong, not because it's complicated, but because they don't know what questions to ask. I help relocating buyers from California every week. I'll walk you through exactly what your California equity gets you in Broomfield, which community fits your lifestyle and budget, and what the real total cost of ownership looks like (HOA + metro district + property tax + mortgage, all in one number).

📧 Email Nick directly: NickAhrensRealestate@gmail.com

🏠 Browse listings: zillow.com/profile/NickAhrensRealEstate

🌐 More guides: youranthemhome.com

Nick Ahrens is a Broomfield real estate expert with the North Denver Report, specializing in Anthem, Anthem Highlands, Baseline, and the North Denver metro.

Frequently Asked Questions

How much equity does the average California homeowner have? As of Q3 2025, the average California homeowner with a mortgage holds approximately $603,000 in home equity, more than double the national average of $299,000 and second only to Hawaii. (Source: Cotality Homeowner Equity Report, Q3 2025)

Can I use my California home equity to buy a house in Colorado? Yes. The most common approach is to sell your California home, net the equity, and use it as a large down payment or all-cash purchase in Colorado. Many Bay Area homeowners can purchase in Broomfield outright with no mortgage. The median home in Broomfield is approximately $647,000 (Zillow, early 2026), compared to $1.5M+ in San Francisco.

Do I pay California taxes when I sell my house and move to Colorado? If you've lived in your California home for at least 2 of the last 5 years, you qualify for the federal capital gains exclusion: $250,000 single / $500,000 married. Gains above that may be subject to California state income tax if you're still a California resident at closing. Timing your residency change before the sale can significantly reduce or eliminate that state tax. Talk to a CPA specializing in interstate relocation.

What is a bridge loan and do I need one? A bridge loan lets you borrow against your California equity to buy in Colorado before your California home sells. It eliminates the need for a contingent offer, a major advantage in a competitive market. Bridge loans typically carry rates 1–2% above standard mortgages and run 6–12 months. Once your California home closes, you pay the bridge off.

What are the best Broomfield neighborhoods for California buyers with significant equity? Anthem (median ~$1,027,238), Anthem Highlands (~$615,000), and Baseline (~$566,000) are the three master-planned communities that attract the most California transplants to Broomfield. All three offer mountain views, strong schools, and resort-style amenities. Read the full community comparison here.