California Capital Gains Tax When You Sell and Move to Colorado: The 3 Surprises Sellers Miss in 2026

Last Updated: May 2026

California Capital Gains Tax When You Sell and Move to Colorado: The 3 Surprises Sellers Miss in 2026

If you sell a California home and move to Colorado, you can usually exclude up to $500,000 of gain (married filing jointly) under IRS Section 121. Anything above that is taxed by California as ordinary income at rates up to 13.3%, and California requires escrow to withhold 3.33% of the gross sale price at closing. Moving to Colorado before you sell does not eliminate the California tax, because California taxes real estate gains by source, not by where you live.

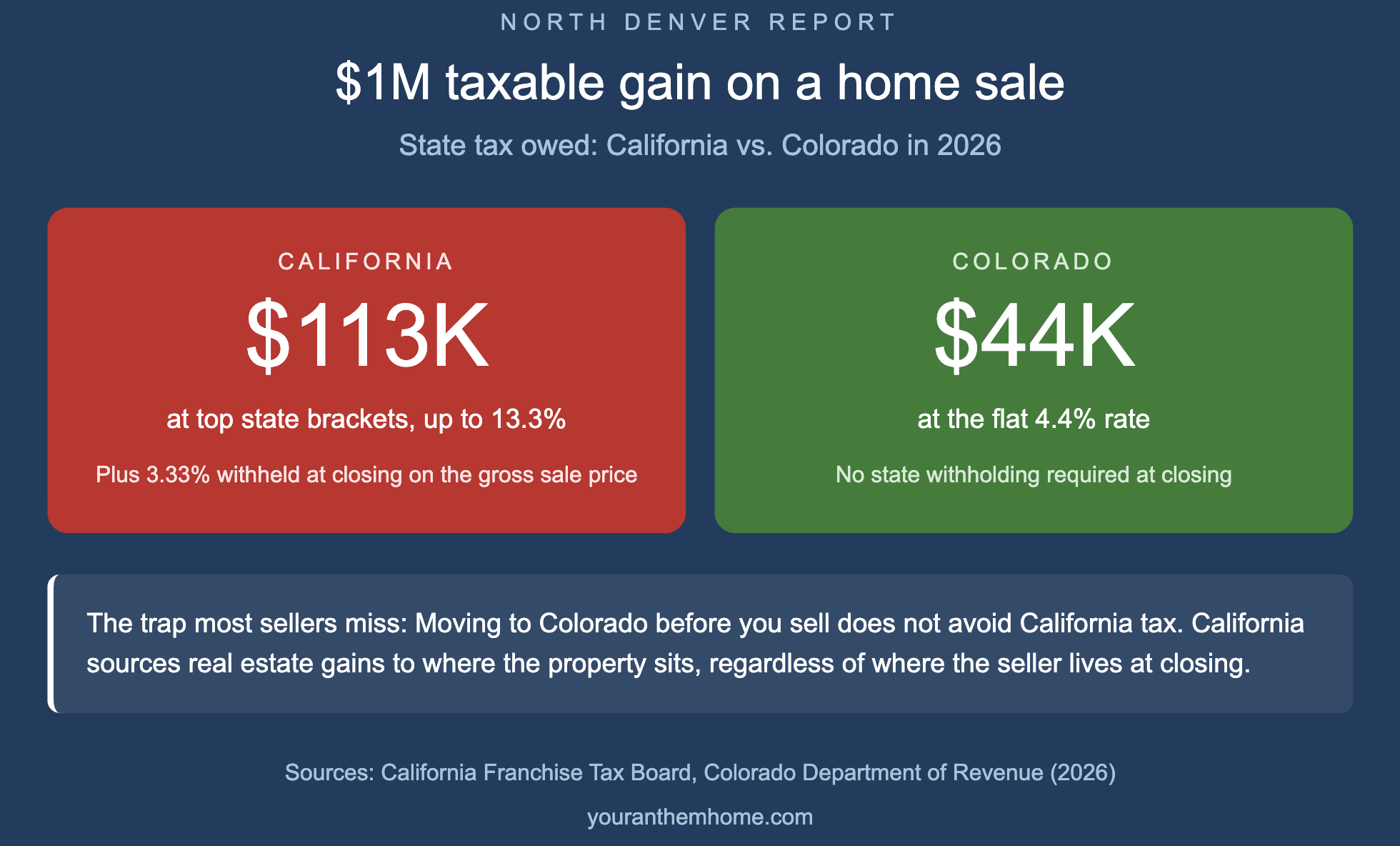

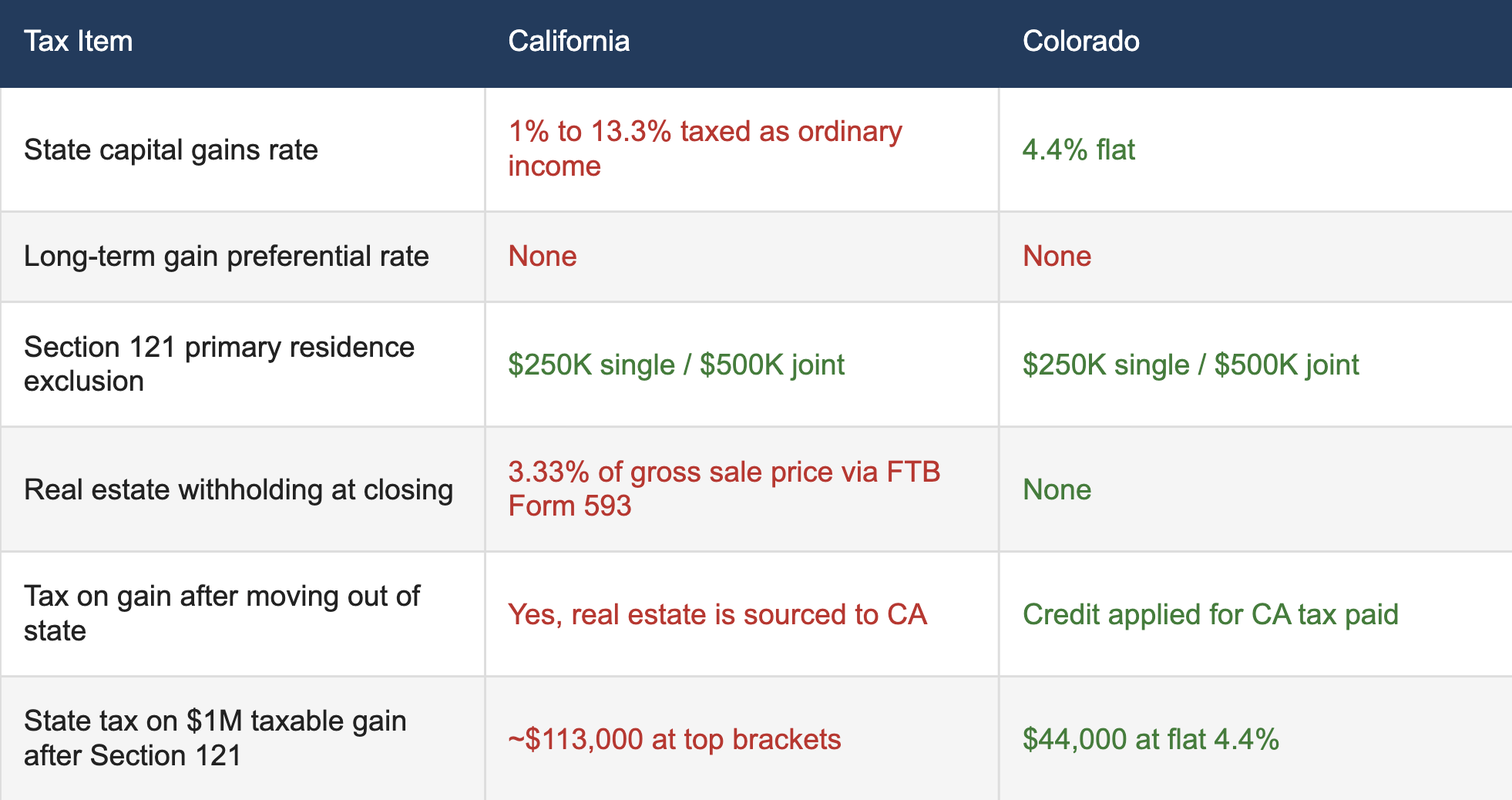

California taxes capital gains as ordinary income with no preferential long-term rate, with brackets running from 1% to 13.3% for tax year 2025 according to the California Franchise Tax Board. The 13.3% top rate applies to taxable income above $1 million and includes the 1% Mental Health Services Tax. Colorado, by contrast, applies a flat 4.4% rate to all taxable income, including capital gains, per the Colorado Department of Revenue. On a $1 million taxable gain after the federal Section 121 exclusion, that rate gap is roughly $89,000 in state tax owed.

I have closed over 350 transactions for clients moving between California and the North Denver metro since 2011, and the same three surprises come up almost every time. Here they are.

Surprise 1: California Withholds 3.33% of Your Gross Sale Price at Closing

When you sell California real estate, the escrow company is legally required to withhold 3.33% of the gross sale price and send it to the California Franchise Tax Board as an advance payment toward your state capital gains tax. The full name of the form is FTB Form 593, Real Estate Withholding Statement.

The math is brutal on a typical Bay Area sale. On a $1.5 million home, that is $49,950 held back at closing before you ever see your equity. On a $2 million Orange County or San Diego home, it is $66,600. The withholding is on the gross sale price, not the gain. So even sellers who owe little or no actual capital gains tax can have tens of thousands of dollars trapped at closing for months.

The fix exists, but you have to file for it. If your gain is fully covered by the Section 121 primary residence exclusion, you can certify that on Form 593 and the withholding is waived. If your gain is partially covered, you can elect to have the withholding calculated on the actual taxable gain instead of the gross sale price. Most California title companies will hand you Form 593 at signing without explaining either election. Do not sign it blank.

Surprise 2: Moving to Colorado First Does Not Avoid California Tax on the Sale

This is the most expensive misconception I see. Sellers think if they buy in Anthem or Anthem Highlands, change their driver's license, register to vote in Colorado, and then sell their California home, the gain becomes Colorado-source income taxed at 4.4% instead of California's higher rates.

That is wrong. California taxes real estate gains based on where the property is located, not where the seller lives. The Franchise Tax Board treats the sale of California real estate as California-source income for nonresidents. You file a California nonresident return (Form 540NR) reporting the gain, and California taxes it at the same rates a resident would pay, up to 13.3%.

Colorado will then tax the same gain as a Colorado resident, but you get a credit for tax paid to California, which usually zeroes out the Colorado portion since California's rate is much higher. The practical result: you pay California rates on the California real estate gain regardless of when you cross the state line. The timing decision should be driven by market conditions, financing, and logistics, not by trying to dodge California tax that California is going to collect anyway.

Surprise 3: California Has No Preferential Long-Term Capital Gains Rate

Federal tax law gives long-term capital gains (assets held over one year) a preferential rate of 0%, 15%, or 20% depending on your income. California does not. California treats every capital gain as ordinary income, no matter how long you held the property, taxed at the regular state brackets up to 13.3%.

For a married couple selling a Bay Area home with $1.5 million in gain after the $500,000 Section 121 exclusion, that means $1 million of taxable gain hits California at the top brackets. The combined federal plus California marginal rate on that gain runs over 33%. The same gain in Colorado would be taxed at a flat 4.4% on the state side. On $1 million of taxable gain, the state-tax difference between selling as a California resident and (hypothetically) being able to source the gain to Colorado is about $89,000. The tax is real, the math is brutal, and the Section 121 exclusion is the single most important number in the entire transaction. Protect it.

How the Section 121 Exclusion Works for California Sellers

The Section 121 exclusion is the federal rule that lets you exclude up to $250,000 of gain (single filers) or $500,000 (married filing jointly) on the sale of a primary residence. California conforms to it, so the same exclusion applies on your California return.

To qualify, you must pass two tests: the ownership test (you owned the home for at least 24 months out of the 5 years before the sale) and the use test (you used it as your primary residence for at least 24 months out of those same 5 years). The 24 months do not have to be consecutive. You can also use the exclusion on a new home every 2 years, so this is not a once-in-a-lifetime benefit.

Partial exclusions exist for sellers who fall short of the 24-month threshold due to a job relocation (the new job must be at least 50 miles farther from the old home than the previous commute), a qualifying health event, or unforeseen circumstances. The IRS calculates the partial exclusion as a fraction of the standard limit based on how long you actually lived in the home.

What Happens When You Move to Colorado: The Part-Year Residency Year

The year you actually move is the most complex tax year of your life. You will likely file a California part-year resident return (Form 540NR) and a Colorado part-year resident return (Form 104PN) for the same tax year.

Income earned while you lived in California gets taxed by California at California rates. Income earned after you established Colorado residency gets taxed by Colorado at 4.4%. Your California real estate sale, regardless of when in the year it closes, gets taxed by California because the property is California-source. If the sale closes after you became a Colorado resident, Colorado will also include the gain on your Colorado return, but you take a credit for the California tax paid, which generally eliminates the Colorado portion.

There is one timing wrinkle worth knowing. If you have other large income items like RSU vesting, exercising stock options, or a bonus, the residency date matters a lot for those. Talk to a CPA about ordering the closing of your California home, the sale of stock, and the date you officially establish Colorado residency. The real estate piece is fixed by source, but the rest of your income is not.

Why Sellers Are Choosing Anthem, Anthem Highlands, and Baseline

The three Broomfield communities I work in most often are the natural landing spot for California sellers. Anthem has a median sale price around $1.03 million, Anthem Highlands averages roughly $615,000, and Baseline runs about $566,000. A California seller with $1 million in net equity after taxes can buy outright in Anthem Highlands or Baseline and still have meaningful cash left over.

The tax reframe goes beyond capital gains. Colorado has a 4.4% flat income tax versus California's progressive 1% to 13.3%. Colorado property tax is roughly 0.5% of assessed value, one of the lowest in the country. California property tax is capped by Proposition 13 but applies to a much higher base, so transplants who bought California homes recently were often paying more in absolute dollars than they will in Broomfield even on a similarly valued home.

For comparison-shoppers, I have a separate breakdown of the California-to-Colorado equity transfer math and a head-to-head Anthem vs. Anthem Highlands vs. Baseline comparison covering price, HOA, schools, and lifestyle.

What If the Property Is a Rental, Not My Primary Residence?

The Section 121 exclusion only applies to primary residences. If you are selling a California rental or investment property, you do not get the $250,000 / $500,000 exclusion. You owe federal capital gains tax (0%, 15%, or 20% depending on income), California ordinary-income rates up to 13.3%, depreciation recapture at up to 25% federal, and the 3.33% FTB withholding still applies at closing.

The main planning tool for investment property is a 1031 exchange, which lets you defer the capital gains tax by reinvesting the proceeds into another like-kind property within strict timelines (45 days to identify, 180 days to close). California has its own clawback rules on 1031 exchanges that move proceeds out of state, which is a separate conversation. If you own a California rental and are thinking about Colorado, email me and I will walk you through the structure.

The Bottom Line for California Sellers Moving to Colorado

Three things to lock in before you list your California home:

First, confirm your Section 121 eligibility. If you have owned and lived in the home for 24+ months out of the last 5 years, the first $500,000 of gain (joint) or $250,000 (single) is excluded from both federal and California tax. This is the single biggest number in the deal.

Second, plan for the FTB Form 593 withholding. Read the form before signing. If your gain is fully covered by Section 121, certify the exemption and avoid the 3.33% withholding entirely.

Third, do not assume moving to Colorado first changes your California tax. The gain on California real estate is California-source income regardless of where you live at closing. Plan around that fact, not against it.

Once you have the California side handled, the Colorado side is the easy part. Flat 4.4% income tax, low property tax, and a buy-side market in Broomfield where your California equity goes considerably further than it did at home.

[INSERT CTA]

Thinking about a move to Broomfield?

I answer every message myself, usually same day.

📱 Text Nick: 949-230-3625

📧 Email: NickAhrensRealestate@gmail.com

🏠 Browse homes: youranthemhome.com/home-search

⭐ Reviews: zillow.com/profile/NickAhrensRealEstate

Frequently Asked Questions

Do I owe California capital gains tax if I move to Colorado before selling my home?

Yes. California taxes capital gains on California real estate based on where the property is located, not where the seller lives. If your home is in California, the gain is California-source income and remains taxable by California even if you established residency in Colorado before closing.

What is the California 3.33% real estate withholding?

California requires escrow to withhold 3.33% of the gross sale price at closing as an advance payment toward potential state capital gains tax. Sellers can reduce or eliminate the withholding by filing FTB Form 593 and certifying that the gain is fully covered by the Section 121 primary residence exclusion.

How much capital gain is excluded when selling a primary residence?

Under federal Section 121, single filers can exclude up to $250,000 of gain and married couples filing jointly can exclude up to $500,000 of gain on the sale of a primary residence. California conforms to these federal exclusion amounts. To qualify, you must have owned and used the home as your primary residence for at least 24 months out of the 5 years before the sale.

What is California's capital gains tax rate compared to Colorado?

California taxes capital gains as ordinary income at rates from 1% to 13.3%, with the 13.3% top rate applying to taxable income over $1 million. There is no preferential long-term capital gains rate at the state level. Colorado taxes capital gains at a flat 4.4%, the same rate that applies to ordinary income.

Should I sell my California home before or after moving to Colorado?

For California real estate, the timing of your move does not change your California tax liability because California taxes the gain by source. The home is in California, so California taxes the gain regardless of when you cross the state line. The decision is usually driven by logistics, market timing, and financing strategy, not state tax savings.